HSN Code & GST for Mobile Phones and Repair Services: Shop Owner’s Guide

What Is an HSN Code and SAC Code? (Quick Answer)

HSN (Harmonized System of Nomenclature) codes classify physical goods for GST, and SAC (Services Accounting Code) does the same job for services. For a mobile repair shop, the phones and spare parts you sell get an HSN code, and the repair labour you charge for gets a SAC code. Get this right and your GST returns match your invoices; get it wrong and mismatched HSN/SAC entries are a common reason GSTR-1 data does not reconcile with GSTR-2B/GSTR-3B.

The short version, if you only need one number: the HSN code for mobile phone billing is 8517 at 18% GST, and repair labour uses SAC 9987, typically also 18%. As of 2026 — always confirm current rates on the official GST portal before filing, since rates and thresholds are revised by GST Council notifications.

HSN Codes for Mobile Phones and Common Repair Parts

Under GST’s HSN classification, mobile phones — smartphones and feature phones alike — fall under heading 8517 (“telephone sets, including telephones for cellular networks”), currently attracting 18% GST. This is the code to use if your shop also sells new or refurbished handsets, not just repairs them.

Spare parts are a different story: each part carries its own HSN classification based on what it physically is, not on the fact that it goes inside a phone. In practice, most repair shops encounter:

- Batteries (lithium-ion cells/packs) — generally under heading 8506/8507

- Chargers, adapters and power banks — generally under heading 8504

- Displays, screens and other phone parts/accessories — generally treated under 8517 (as parts of the heading) or the part’s own heading, depending on what it is

Because these headings can have sub-classifications (6-digit and 8-digit codes) that shift with GST Council notifications, treat the above as heading-level guidance, not a final answer for your invoice. Pull the exact code from the GST portal’s HSN/SAC finder, or ask your CA to confirm the precise code for each part you stock — especially before a large inventory import or an HSN summary filing.

SAC Code for Mobile Phone Repair Services

The labour you charge for diagnosing and fixing a phone — screen replacement, battery swap, water-damage repair, software fixes — is a service, not a good, so it is classified under a SAC rather than an HSN code. Repair and maintenance services of goods generally fall under SAC heading 9987 (“maintenance, repair and installation (except construction) services”), which typically attracts 18% GST. This is the code most mobile repair shops should use on the labour/service line of an invoice, whether the repair is billed standalone or alongside parts.

As with HSN, the exact sub-code (6-digit) can vary by the specific nature of the service — confirm with your CA or the GST portal if you are unsure which sub-heading fits your shop’s exact service mix.

GST Rates at a Glance: Phones, Parts and Repair Services

Here is a compact reference for the codes and rates a mobile repair shop deals with most often. Treat every rate below as a starting point — always verify the current rate on the GST portal before you file, since rates change by Council notification.

| Item / Service | HSN / SAC Heading | Typical GST Rate (2026) | Note |

|---|---|---|---|

| Mobile phones (new or refurbished handsets) | HSN 8517 | 18% | Use only if you also sell handsets, not just repair them |

| Repair & maintenance labour (screen, battery, software, etc.) | SAC 9987 | 18% | The default heading for repair-shop service billing |

| Batteries sold as spares | HSN 8506/8507 (heading-level) | Typically 18% | Confirm exact sub-code with your CA |

| Chargers, adapters, power banks | HSN 8504 (heading-level) | Typically 18% | Confirm exact sub-code with your CA |

| Screens, displays & other phone parts | HSN 8517 (parts) or part’s own heading | Typically 18% | Depends on the specific part |

Composite Supply vs Mixed Supply: Billing a Repair Job With Parts

Most repair jobs are not pure labour — you replace a battery, a screen or a charging port, and bill for both the part and the work. GST law has a specific lens for this: when goods and services are supplied together in the natural course of business, with one clearly the main service and the other incidental to it (a broken-screen repair naturally includes fitting a new screen), it is generally treated as a composite supply, taxed at the rate of the principal supply — normally the repair service.

In mobile repair, this rarely changes what the customer pays, because both the parts (18%) and the service (18%) usually sit at the same rate anyway. What it does affect is how you classify and report the transaction — whether you show one combined line at SAC 9987 or itemize the part (HSN) and the labour (SAC) separately. Many repair shops itemize both for clarity to the customer and cleaner inventory tracking, which is fine as long as each line carries its correct code. Where it gets less obvious — extended warranties, bundled accessories, or a repair sold together with an unrelated retail item — talk to your CA; composite-vs-mixed-supply classification has real edge cases that a general guide cannot rule on for your specific invoice.

Input Tax Credit (ITC) for Mobile Repair Shops

If you are GST-registered, you can generally claim input tax credit on the GST you pay when buying spare parts, batteries, screens, tools and other inventory used for your taxable repair business — the credit reduces the GST you owe on your own sales. To claim it cleanly:

- Buy from GST-registered suppliers who issue proper tax invoices with their GSTIN and the correct HSN code for the part

- Make sure your purchases show up in your GSTR-2B (the credit only flows through if your supplier has filed correctly on their end)

- Keep purchase invoices matched to what you actually stock and use in repairs — parts bought but not linked to any business use can be questioned

- Note that ITC generally is not available if you have opted for the GST composition scheme, since composition dealers do not charge or claim GST in the normal way

Getting your purchase-side HSN codes right is not just about compliance — it directly affects whether your ITC claim reconciles automatically or gets stuck in a mismatch you have to chase every filing cycle.

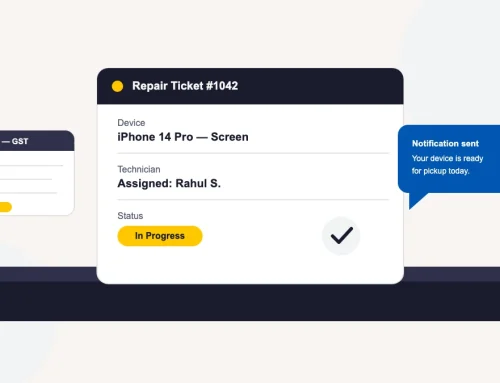

How to Show HSN and SAC Codes on Your Repair Invoices

Every GST invoice a repair shop issues should carry the HSN code against each parts line and the SAC code against each labour/service line — this is what your GST return’s HSN summary is built from. Whether you are required to print the code, and how many digits (4, 6 or 8), depends on your annual turnover; the threshold has changed across past GST Council cycles, so confirm the current requirement on the GST portal rather than going by an old note.

In practice, the operational challenge is not knowing the code once — it is applying it correctly, invoice after invoice, across dozens of different parts and repeat repair jobs. This is where mobile repair shop software pays for itself: BytePhase’s GST-compliant invoicing lets you tag each inventory item and job-sheet line with its HSN/SAC code once, so every estimate and invoice generated from a repair ticket carries the right code automatically instead of being retyped by hand. A ticket moves from diagnosis to estimate to invoice without re-entering line items, parts are tracked by barcode so your stock and your invoice always agree, and the finished invoice can go out to the customer over WhatsApp, SMS or email the moment it is ready. Shops billing at the counter with point-of-sale billing alongside job tickets get the same code discipline there too.

BytePhase is used by 2,000+ repair and service businesses across 32+ countries, and shops can try the full ticketing, inventory and GST invoicing workflow free for 15 days, no card required, before deciding if it fits how their billing already works.

For the reporting side — pulling GST-ready sales and job-sheet data out at filing time — see our related guide on exporting GST reports from BytePhase, or read more on choosing mobile repair software generally.

Common GST Billing Mistakes Mobile Repair Shops Make

- Copying one HSN code onto every invoice line regardless of what was actually sold — a charger and a battery are not the same code

- Leaving the HSN/SAC field blank because “the software did not ask” — most billing tools let you set it once per item, not type it every time

- Billing the full repair as a single unlabelled “service” line, which under-reports the value of parts consumed in GSTR-1

- Assuming a rate learned years ago is still current — GST rates and the HSN/SAC printing threshold have both changed through Council notifications; recheck before every filing season

- Not distinguishing between selling a phone outright (HSN 8517, a good) and repairing one (SAC 9987, a service) — they are taxed under different headings even though a repair shop may do both

- Skipping ITC claims because purchase invoices do not carry a proper GSTIN or HSN code, which blocks the credit at GSTR-2B matching

FAQs: HSN Code and GST for Mobile Repair Shops

Mobile phones — smartphones and feature phones — fall under HSN heading 8517, which currently attracts 18% GST. This applies if your shop also sells handsets, not just repairs them. GST rates are set by Council notification, so always confirm the current rate on the official GST portal (gst.gov.in) before filing.

Repair and maintenance labour for mobile phones — screen replacement, battery swaps, software fixes and similar work — generally falls under SAC heading 9987 (“maintenance, repair and installation services”), typically taxed at 18%. Confirm the exact sub-code with your CA if your shop’s service mix is unusual.

Most mobile repair jobs are treated as a composite supply, taxed at the rate of the principal service (repair, typically 18%) — and since parts also usually sit at 18%, the practical rate rarely changes whether you bill one combined line or itemize parts and labour separately. Bundled accessories or extended warranties are edge cases worth a quick check with your CA.

Under general GST rules, service-led businesses typically need to register once turnover crosses ₹20 lakh (₹10 lakh in special category states), while predominantly goods-based businesses register at ₹40 lakh in most states — a repair-and-parts shop usually falls under the services threshold. These limits are set by notification and can change, so verify the current threshold on the GST portal before assuming you’re under or over it.

Tag each parts line with its HSN code and each labour/service line with SAC 9987 (or the correct sub-code) so your invoice matches what you report in your GSTR-1 HSN summary. Repair-shop billing software like BytePhase lets you set the code once per inventory item and job-sheet line, so every estimate and invoice generated from a repair ticket carries the right code automatically instead of relying on someone retyping it correctly every time.